Repeal

of Glass-Steagall and the Too Big To Fail Culture

During the 1990’s the conventional economic wisdom supported the

repeal of Glass-Steagall. However, "10 years later, the end of Glass-Steagall has been blamed by some for many of the problems

that led to last fall’s (2008) financial crisis. While the majority of problems that occurred centered mostly on the

pure-play investment banks like Lehman Brothers, the huge banks born out of the revocation of Glass-Steagall, especially

Citigroup, and the insurance companies that were allowed to deal in securities, like

the American International

Group, would not have run into trouble had the law still been in place."

This assessment by Cyrus

Sanati, also seems to be the typical perception, now that the anemic rescue of the economy struggles to claw back to pre 2008

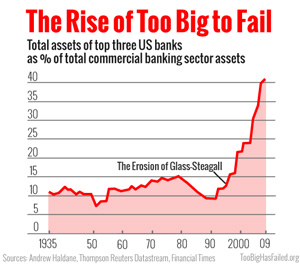

levels. The separation of commercial banks and investment banking was a cornerstone in finance, since the Banking Act of 1933 established a protective firewall. The Corporatocracy culture that operates

as todays dominate economic model, adopts the "Too Big To Fail" paradigm. Tapping an unending stream of capital for acquisitions,

mergers and poison pill financing to fend off unwanted suitors, is a continued requirement to survive in a global investment

environment, where soveriegn wealth funds operate as preparatory pirates.

Commercial

banks once had a clear mission statement and purpose, underwriting business and mortgage loans. Since Investment Banks, now

allowed to access the Federal Reserve discount window programs, because they are now considered depository institutions, the

impact of the repeal of Glass-Steagall becomes evident.

"Lending

at the 12 regional Home Loan Banks rose 30 percent to $492 billion between March of 2013 and December 2013, largely the result

of advances made to JPMorgan, Bank of America Corp., Wells Fargo & Co. (WFC) and Citigroup Inc., according to a report

released today by the Federal Housing Finance Agency Office of the Inspector General.

The

concentration of Home Loan Bank lending in four large institutions could present safety and soundness risks, the report said.

In addition, auditors questioned whether lenders created to support housing finance should be providing funds so banks can

meet standards set under the international Basel III accord."

Now

does anyone seriously expect that the money center banks dedicated their capital to fund mortgages for the masses? The notion

that such mega institutions prefer to function as commercial lenders is a stretch at best. Nevertheless, the investment banking

culture is changing out of necessity. The Volcker rule has taken its toll on the whales of finance.

Over two years ago, the announcement that Citigroup to Close Prop

Trading Desk, was news. Even before that shift, the banksters began plotting to circumvent

the regulator restrictions. "In October 2010, the proprietary trading group at Goldman Sachs left the bank to start a similar operation at Kohlberg Kravis Roberts, the private equity giant. JPMorgan Chase moved its proprietary desk out of its investment bank and into its asset

management unit last year, and Morgan Stanley has said it will spin its proprietary operation into a separate entity later

this year."

A prominent proponent of restoring Glass-Steagall has been the Larouche Pac.

"Glass-Steagall

is the indispensable first step to global economic recovery. It will immediately halt the onset of hyperinflation, remove

government commitment from bailing out toxic debts, end too-big-to-fail banks, and force a separation of commercial banking

functions from investment banking functions, thus cleaning up the nation's banking system to make way for real, long-term

investments.

There are now two bills in each house calling for the

restoration of President Roosevelt's 1933 Glass-Steagall law. H. R. 129 & its Senate companion bill S. 985, introduced by Rep. Marcy Kaptur and Senator Tom Harkin respectively, and

most recently, S. 1282, known as the "21st Century Glass-Steagall Act," championed by

Senator Elizabeth Warren, whose companion House bill, H.R. 3711 was recently introduced on December 11, 2013."

It is disappointing that progressive collectivists are leading the effort

for a return to a law that served well for decades. The absence of bipartisan support is disturbing. Lefty loons embrace Elizabeth Warren for many foolish reasons. In spite of this, her claim that, "Reintroducing

Glass-Steagall will make it so depositor’s money cannot be used for the derivatives market" is a desired objective.

When Yaron Brook and Don Watkins argue in Forbes, Why The Glass-Steagall

Myth Persists, they seem indifferent about accelerating the "Too Big To Fail"

mentality that became the operative political concern, as the megabanks took on more leverage and risk.

"In 1999, President Clinton signed GLB into law. Although it left the bulk of Glass-Steagall in place, it

ended the affiliation restrictions, freeing up holding companies to own both commercial and investment banks.

There is zero evidence this change unleashed the financial crisis. If

you tally the institutions that ran into severe problems in 2008-09, the list includes Bear Stearns, Lehman Brothers, Merrill

Lynch, AIG, and Fannie Mae and Freddie Mac, none of which would have come under Glass-Steagall’s restrictions. Even

President Obama has recently acknowledged that "there is no evidence that having Glass-Steagall in place would somehow

change the dynamic."

Of

course, the establishment political class would never admit that their financial donors and patrons must hinder their unbridled

trading strategies. The point of the proposed bill, 21st Century Glass-Steagall

Act of 2013 or any other legislation that attempts to

reign in the excesses of the banking system is that the political will is entirely absent to go against the banksters. Enactment

of an updated Glass-Steagall is certainly not the definitive answer to an unsustainable debt ridden financial fiat banking

system. Yet, where does one start to build public critical mass to replace the private Federal Reserve monopoly on money,

with economic commerce, that is not the prisoner of banking exploitation? The disastrous institution that fails us all is

the current banking cartel.