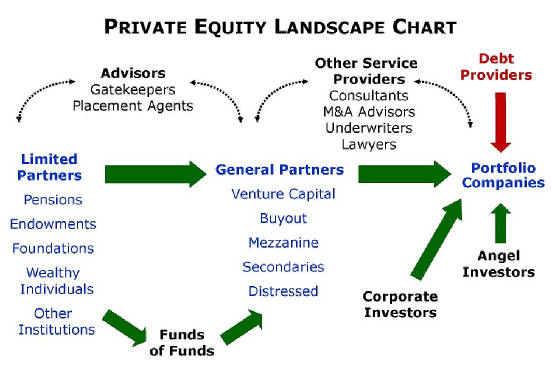

Private Equity a Formula for Fraud

How quaint, private equity sounds like the very definition

of capitalism. Well, peel back this onion and the tears come streaming from your eyes. As with any insider investment scheme,

the devil is in the details. So when these operations fell under government regulation, some optimists felt good that the

government would protect the limited partners and the entire financial system. Just how did it work out?

Mike Konczal reports in The SEC Has Revealed Astounding Corruption in Private Equity.

“As

a result of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act, private equity firms must register with the

Securities and Exchange Commission (SEC). This, in turn, allows the SEC to examine the behavior of private equity firms on

behalf of investors. The SEC just completed an initial wave of 150 firms, and what it found is shocking.

These results were unveiled last week when Andrew

Bowden, the director of the SEC’s examinations office, gave a speech titled “Spreading Sunshine in Private Equity.”

The big takeaway: Half of the SEC’s exams find corruption in the way fees and expenses are handled. Or as Bowden forcefully

describes it: “When we have examined how fees and expenses are handled by advisers to private equity funds, we have

identified what we believe are violations of law or material weaknesses in controls over 50 percent of the time.”

As any seasoned player in the equity markets understands,

the fees charged to play the game can rapidly eat up any marginal profits and have a drastic negative effect on total returns.

Naked Capitalism provides the following in the article,

Carlyle, Apollo, Blackstone Cheat Private Equity Investors with Legal Fee Ruse.

“Gretchen Morgenson at the New York Times describes how private equity firms arbitrage legal fees. They dispense so much in the way of legal fees, between buying and

selling companies, arranging for financing, and raising funds, that they are the most sought-after clients of big law firms

and accounting firms. That means they are in a position to obtain discounts.

But guess what? The only beneficiary of the private equity firms’ buying

power in too many cases is the private equity firm itself. The general partners get a break for themselves, on the back of

the vastly greater dollar value of fees generated at the portfolio company and limited partnership level. The investors pay

the rack rate or even a premium.”

Abuses

in the private equity structure have long been alleged. Finally a research study adds evidence to this issue. Read the entire

White Paper on Addressing financial fraud in the private equity industry.

“This

paper addresses the more prevalent areas where private equity firms, brokers and other advisers may be subject to accusations

of manipulation or fraud. Certain characteristics of the private equity industry may make it more susceptible to allegations

of fraudulent activities, such as relatively long lockup periods, illiquid investments, complex transactions, broad partnership

agreements, a perceived lack of transparency, inherent conflicts of interest and activist investors. Investors are scrutinizing

the performance and activities of their portfolio managers, financial advisers, agents and the portfolio companies themselves.

Limited partners are increasingly more critical of disclosure materials supplied by general partners and are demanding more

detailed performance data.

Stakeholders must be prepared to respond to issues that may arise at both the fund management and portfolio company

level. Stakeholders must also provide careful oversight of their outside financial advisers, brokers and other agents.”

For those with brave hearts and deep pockets, joining

a private equity fund as a limited partner carries with it the ultimate disclaimer, caveat emptor. The standard 2 and 20 Private Equity Fee Structure is being challenged. However, the gimmicks and tricks used to siphon off the top costs to fund a crony insider get rich scheme

is expected from the “Masters of the Universe”.

A list of the 100 Best-Performing Hedge Funds places D.E. Shaw as the fifth most profitable fund. Examining the kind of swindles employed for ripping off public funds

to line the pockets of connected political cronies is provided in the article, Industrial Wind and the Wall Street Cap and Trade Fraud.

Folks, such strategies are a far cry

from buy, hold and collect dividends model.

The

hedge fund desperados are slick con operators who talk fast, bribe politicians, circumvent legal restrains and outright lie

about the nature of the businesses they promote, while manipulating their equity price. One such study asks, Do Hedge Funds Manipulate Stock Prices? The abstract conclusion suggests:

“We provide evidence suggesting that some hedge funds manipulate stock prices on critical reporting

dates. Stocks in the top quartile of hedge fund holdings exhibit abnormal returns of 0.30% on the last day of the quarter

and a reversal of 0.25% on the following day. A significant part of the return is earned during the last minutes of trading.

Analysis of intraday volume and order imbalance provides further evidence consistent with manipulation. These patterns are

stronger for funds that have higher incentives to improve their ranking relative to their peers.”

Building great fortunes like the 40 richest hedge fund managers departs from the old formula of actually creating real productive economic business ventures. All of these billionaires

share a common connection in using and leveraging the financial system for the benefit of the hedge funds “godfather”,

usually at the expense of the general public.

Note that few of these hedge fund gurus are household names. The one obvious exception is the richest operator at

24.4 billion, George Soros.

The decades of looking the other way

that allowed the predatory class from enriching their financial worth has a direct connection with the benign neglect from

government regulators who lust for a chance to earn upward mobility through the revolving door of assisting the hedge fund

community.

The rot on Wall Street is clearly

demonstrated by the modus operandi of the hedge fund titans. Dodd-Frank has failed. It is time to reel in the rackets.

James Hall – June 17, 2015

Subscription sign-up for the BATR RealPolitik Newsletter

Discuss or comment about this essay on the BATR Forum