The

primary players that caused the housing bubble are:

1)

The banking institutions that bundled and sold very risky mortgages

2) The Wall Street firms that bought these instruments and hedged for a default hazard by booking speculative derivative

insurance that could never pay off on massive defaults

3) Fannie

Mae and Freddie Mac provided government backing, of last resort, on bad mortgages

In order to understand the how this came about, one needs to acknowledge the role of repealing the Glass-Seagall Act. In the account, Repeal of Glass-Steagall Act cause

of housing boom, the conclusion is evident.

"The purpose of the Glass-Steagall Act was to control speculation and prohibit a bank from owning other financial

institutions which would create a conflict of interest, such as investment banks and insurance companies. The Glass-Steagall

Act was enacted in 1933 after excessive risk-taking that contributed to the Great Depression. Jean-Marie Eveillard, of First

Eagle Funds, has said: "Glass-Steagall protected bankers against themselves. Bankers are sheep. They don't mind going

over the cliff if everyone else goes over the cliff."

The reason banks were giving out such risky loans is that they were able to securitize them and sell them as mortgage

backed securities and other collateralized debt obligations to investors. With the ability to both create loans and then underwrite,

securitize and sell mortgage backed instruments under one roof, it is easy for banks to create a ponzi-like scheme."

"The

truth is that high-risk mortgages were "bundled" just like good mortgages and sold as iron-clad securities. Accounting

practices allowed banks to "book" profit from these loans immediately and account for the risks later. The same

practices were used on the infamous "credit default swaps." These are insurance-like contracts that promise to cover

losses on certain securities in case of a default—except they didn’t always work that way in the unregulated credit

swaps market.

This created the short-term results that shareholders

demanded. Could bank executives have booked less profit and held some reserve for the rainy day that was sure to come? Sure,

and they would have been fired. The shareholders would have demanded they be replaced by their colleagues who were willing

to show higher profit. So the money was taken as profit years ago, and there’s nothing left but debt."

Politicians like Barney Frank advanced the utopian notion that even the most financially

destitute deserve to own a home. Having the ability and income to make mortgage payments seems foreign to the social engineers.

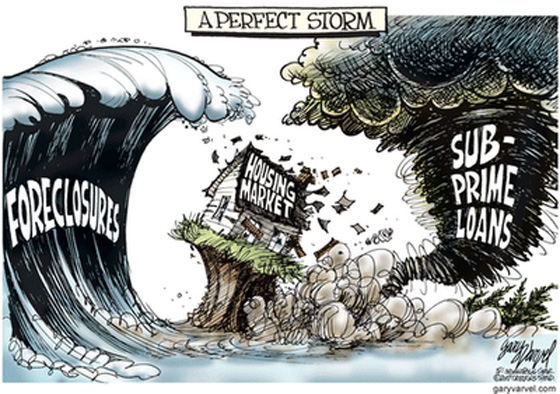

The government rescue net would fix any cracks in the money tree. Add the practice of packaging subprime mortgages and you

have the perfect storm. The collapse of the housing market is a direct result of unrealistic expectations, unreasonable low

interest rates and unlimited loans provided to unqualified borrowers.

The beleaguered mortgagor shares in the dislocation, when their dream of home ownership is stripped. Evictions are

postponed for humanitarian reasons as unwinding of the financial markets drag on for years. Even historically low interest

rates cannot prime the pump any longer.

The fair value for

housing must have a reasonable collation to actual replacement costs. Yet a property is only worth a price that a buyer is

willing to pay. The idea that securing financing of underwater properties, when current owners or fresh buyers can

no longer qualify for a new mortgage, smacks of a designed policy to depress real estate values for years to come.

The draconian Dodd-Frank Act just added more layers of punitive regulations that

adversely affect prospective buyers, while avoiding the needed rational regulations that would restore the separation that

Glass-Steagall protected for decades.

•The key flaw in the Dodd-Frank Act

(DFA) is its effort to control the quality of mortgages by imposing regulation and regulatory costs on lenders and securitizers.

•Because it focuses on only a narrow part of the mortgage

market, and exempts the government-backed sectors, the act will do nothing to prevent the deterioration in mortgage underwriting

standards.

•A plan developed at AEI would define a "prime

mortgage" by statute, making it possible to eliminate the qualified mortgage, the qualified residential mortgage, and

the 5 percent risk retention.

•The fundamental flaws in

the housing finance provisions of the DFA cannot be repaired by regulation; they should be repealed and replaced by the plan

developed at AEI.

In late March, the bank and securities

regulators charged with filling in the details of the DFA's provisions on mortgage-market reform released a set of proposed

rules outlining how the act's broad terms will likely be implemented. The reaction in the market was something close to shock,

as mortgage bankers, mortgage insurers, securitization specialists, and even the Center for Responsible Lending panned the

rules in testimony before the House Financial Services Committee.

Examine

the details of the AIE alternative on their web site that presents their plan.