If

your Main Street business needs capital and seeks a loan, your prospects are slim to none. It is evident that the real economy

has never recovered from the collapse of the financial system. TARP was a temporary rescue of the large money center banks.

For the local community banks, the massive give away has strings attached and penalties to be paid. Not much consolation for

a small business endeavor that is desperate for cash and an improved business environment.

"Hundreds of small banks can't afford to repay federal bailout loans, a top watchdog

will warn Wednesday in a report that challenges the government's upbeat assessment of its financial-system rescue.

Christy Romero, special inspector general for the Troubled Asset Relief Program, said 351

small banks with some $15 billion in outstanding TARP loans face a "significant challenge" in raising new funds

to repay the government."

Slow economic activity results

in the inability to service previous debt loaned by small banks. Without a meaningful recovery, the harsh reality existing

is that a run on bank defaults will begin. Even under this bleak threat, local banking has continued to do the yeoman’s

work to keep essential businesses operating.

Contrast this effort with

the utter neglect and absence of the mega banks from engaging in their chartered purpose of making commercial loans. The too

big to fail cabal has miserably failed the domestic economy. If you believe Frontline’s Astonishing

Whitewash of the Crisis you will never appreciate the ruthless nature of the Big Bank culture.

The PBS Frontline series "Money, Power, and

Wall Street.", Part II is worth viewing to understand the methods used to conceal the systemic

abuses of the post Glass-Steagall era. The first two parts of the four part series recently aired. "The first segment

is particularly troubling. It heavily cribs from the Gillian Tett book Fool’s Gold." The critique concludes, "So thus far, we have some populist

decorating of a profoundly pro-Establishment account."

The

negative review based on a viewpoint that concealing the rudimentary problems of the speculative mortgage scheme gamble is

no solution for resolving the horrific consequences of mixing investment banking with making commercial loans.

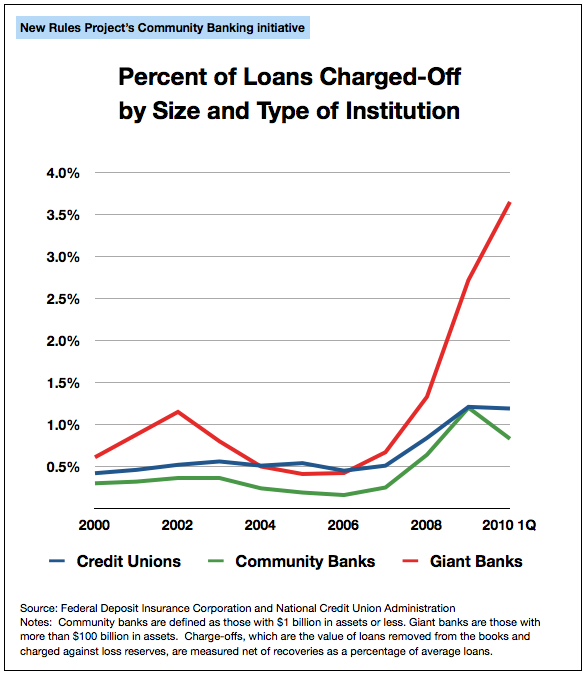

When the Fed bailed out the Big Banks, the money went to cover the losses from derivative

speculation and trading. These exotic financial instruments are all smoke and mirrors. The Big Banks charged off huge sums.

Still much of their toxic assets remain on their books in one form or another. Compare these losses with the more responsible

management from credit unions and community banks. (see chart)

Low

Fed funds benefits money center banks as a lifeline because they were the financial institutions that booked the largest bets.

The intentional bailout that rewarded irresponsible behavior is proof positive that the banks that are the owner of the private

Federal Reserve, dictate financial policy to the Treasury.

"While large banks have successfully exited the TARP program

and returned to "high-risk behavior", the report said that "after 3½ years, community banks have an

uphill battle to exit TARP because they cannot find new capital to replace TARP funds."

The net result translates into withdrawing the ability and willingness to support main street

businesses with fresh credit. The WSJ article continues,

"The

struggling banks are unlikely to find any help on Capitol Hill. Rep. Scott Garrett (R., N.J.), a TARP critic, called the plight

of the small banks another example of how "ill-conceived" the rescue was in the first place.

"It was not thought through as to how it would be implemented... it was not thought

through how they're going to extricate themselves," he said."

The

money centered banks view small business as incidental to the global economy. The corporatist culture creates a total infusion

of big banking and transnational companies into a virtual crime syndicate. The domestic economy that keeps the declining middle

class employed suffers dramatically under this model. Ordinary citizens relegated to the mercy of government "safety

net" programs, experience a lower standard of living. Independent enterprises fail, because credit withdrawn from the

small banks, results in diminished lending.

Small business produces

most of the employment. Access to credit is a necessary requirement for cash flow needs and prudent growth. When the large

banks ignore the financial needs of employer owned businesses, community banks lack the liquidity to fund and support their

needs. This is a designed policy to wreck the national economy.

The

Federal Reserve lends to the money-centered banks at next to zero, while their trading desks scheme to rebuild their balance

sheet. In the process, avoiding direct lending, as too risky, becomes the excuse. Lavish salaries and large bonuses enhance

the moneychangers, while the local merchants go out of business because they cannot fund their operation.

Those who defend an internationalist corporate centered economy, view our neighbors as collateral

damage. Main Street is unnecessary to the titans of global capital. Bankruptcy and foreclosures of the little people are simply

statistics to the elites.

Costly credit card and revolving loans is a

sure path to the poor house. Entrepreneurship is impossible without access to money. As long as Wall Street targets community

banks for extinction, the prospect for small business is bleak. Forget about a broad base economic recovery. Future bailouts

for the influential banksters are inevitable as long as this inept abandonment of local communities continues. This David

vs Goliath saga is an essential struggle against the Philistines. "Too Big to Fail" is a formula for national suicide.