|

Revenue Budget Projections

The

Obama administration is looking for any good news as their culture of scandals unravels. What better economic development

than a reduction in deficit finances for a breath of fiscal cheer. The essential questions that persist about a stalled economy

and a suffering middle class still are unanswered. In addition, the premise that raising taxes, especially on the besieged

tax payer, is a productive method to close the gap on public spending, is simply more of the same flawed policy that contributes

to the increase in the national poverty level. When the Congressional

Budget Office issues their Updated Budget Projections:

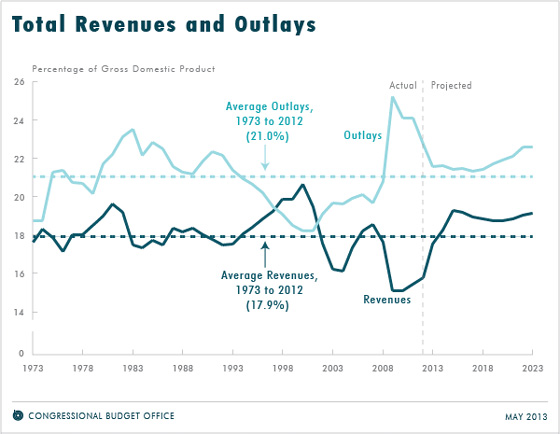

Fiscal Years 2013 to 2023, the assumption that spending will not increase is about as plausible as

a dramatic reduction in food stamps is probable. "If

the current laws that govern federal taxes and spending do not change, the budget deficit will shrink this year to $642 billion,

CBO estimates, the smallest shortfall since 2008. Relative to the size of the economy, the deficit this year—at 4.0

percent of gross domestic product (GDP)—will be less than half as large as the shortfall in 2009, which was 10.1 percent

of GDP. Because revenues, under current law, are projected to rise more

rapidly than spending in the next two years, deficits in CBO’s baseline projections continue to shrink, falling to 2.1

percent of GDP by 2015. However, budget shortfalls are projected to increase later in the coming decade, reaching 3.5 percent

of GDP in 2023, because of the pressures of an aging population, rising health care costs, an expansion of federal subsidies

for health insurance, and growing interest payments on federal debt. By comparison, the deficit averaged 3.1 percent of GDP

over the past 40 years and 2.4 percent in the 40 years before fiscal year 2008, when the most recent recession began. During

the next 10 years, both revenues and outlays are projected to be above their 40-year averages as a percentage of GDP."

To the extent that borrowing less is real, not everyone believes it is desirable. From the

Christian Science Monitor, Federal deficit falling

fast: Is that a good thing ... or a bad thing? "The federal government

is on track to spend $82 billion less this year than last year, while pulling $363 billion more in tax revenue out of consumer

wallets. "The [deficit] is coming down too fast given the still weak

economy," says Jared Bernstein, an economist and former Obama administration adviser, in his blog."

Pray

tell, the Keynesians are coming back out of the closet once again now that sequester-related spending cuts start going into

effect. When will big government proponents celebrate the first positive reduction in the growth of federal spending? A more balanced assessment follows: "A USA Today poll of economists in February found that many see long-term deficit reduction

as a plus for the economy in the short run. Fully 9 in 10 said that, if a "grand bargain" on deficit reduction is

reached, it would make the economy at least somewhat stronger next year."

The quest for a "grand bargain"

on a total revamping of the federal tax code that rejects the failed record of social engineering and corporate welfare would

be the most productive development in monetary sanity since the FDR era. As starved as the taxpayer is for a semblance of optimism in the financial health of the economy, the money-spinning

drag coming out of a federal government godfather, is a fundamental reason why private enterprise is unwilling to take the

risk of business expansion. As long as the consumer is unemployed or fearful of losing their part time job, how is it possible

to ramp up the productive side of the equation, when higher taxes are expected from Obamacare? "Not

only was inflation higher in the 1980s and 1990s than is currently projected for the next decade, real interest rates (nominal

rates adjusted for inflation) were also higher during those periods than in CBO’s baseline projections for the coming

decade. If real interest rates over the next decade ended up matching those historical values, it might be because the economy

(and thus demand for credit) was stronger than in CBO’s projections. In that case, revenues would be greater than the

amounts projected in the baseline, offsetting some of the increase in interest costs."

What kind of distorted world do the bureaucratic inbreeds populate? Any consumer

who visits a supermarket knows all too well that inflation is dramatically higher than that reported in government projections.

Nevertheless, assuming CBO estimates, the Wall Street Journal in, If Rates Rise, Larger Deficit Follows, offers a fateful warning.

"If interest rates rise to the averages

seen between 1991 and 2000 — that is, 4.9% on the 3-month Treasury bill and 6.7% on the 10-year Treasury note in 2023

— then the deficit would be $274 billion bigger in that year than it would otherwise be — and $1.44 trillion bigger

over 10 years. Or, in a slightly different scenario, if interest

rates rise as the highest 10 predictions of the private-sector economists surveyed by the Blue Chip Economic Indicators —

that is, 4.5% on the 3-month Treasury and 5.8% on the 10-year in 2023 — then the federal deficit will be $157 billion

bigger in that year then it would otherwise be, and $1.14 trillion bigger over ten years." The WSJ conclusion: "But the point is clear: A government that borrows

a lot will spend a lot more on interest when rates return to normal."

Even if you want to believe in the official projections, events have a way of going

from bad to worse. La La Land has a talent of fostering "good government" for the political class. The rest of us

are left to pay the interest on their deficit spending. James

Hall – May 22, 2013

Discuss or comment about this essay on the BATR Forum

|