|

Bond

Bubble Expectations

Bonds

are loans that have the expectation of payback with interest. Government bonds are viewed as the safest financial instrument

since the primary fiscal obligation of the state is to honor the terms of their own notes. However, in the fevered climate

of currency wars among central banksters, the security factor of capital repayment is rapidly coming into question. As interest

rates rise, the economic value of the bond diminishes. This inverted normal relationship is the essential dynamic of lending

money with the purchase of Treasury Bonds. So what is all the talk about a bond bubble and likelihood that it will destroy

your underwriting capital? Bloomberg Businessweek warns in the article,

The Rising Bubble in Bond-Bubble

Chatter. "An

asset price bubble is when the expectation that the price can only go higher forms the only rationale for purchase,"

remarked BlackRock’s (BLK) bond honcho Jeffrey Rosenberg Thursday at the CFA Society of Los Angeles’s Economic

& Investments Forecast Dinner, at which the "wherefore bond bubble" discussion dominated. "But the main

motivation of investors for buying fixed income is the opposite of typical bubbles—the fear of losing money rather than

the greed of potential profit has fueled the historic shift of assets into fixed income."

Just how safe is your money when you are holding T-Bonds? The U.S. Treasury wants you to

believe that no other form of currency has the protection of first guarantee of the full faith and credit of your own government.

Well, the mere questioning of this mythical assurance breeds deep distrust and instability of confidence into the entire fiscal

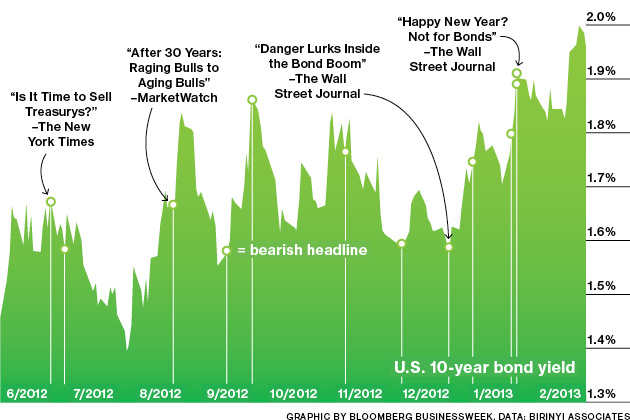

system. Morningstar offers an assessment in The Bond Bubble Threat, which on the surface is very sensible. "To understand the implications of where we are, consider the history of the benchmark

10-year Treasury note. From 1900 to 2012, the average interest rate (yield) was 4.99% (often quoted as 5%). On Jan. 30, 2013,

the yield was 1.99%, well below the long-term average. The prime interest rate, which the Fed has a role in setting, is 3.25%.

It is the break-even rate for banks pricing loans. When the performance

of an asset class runs substantially above or below a long-term average, the odds increase that at some point performance

will move back toward the long-term average. It may take a while for the interest rate on 10-year Treasury paper to re-approach

5%, but at some point, it will. As interest rates creep up, we see a shift away from fixed debt instruments to variable rate

paper, stocks and various inflation hedges."

Regretfully,

when was the last time that economic fundamentals applied to the money debasement manipulations of the Federal Reserve? No

doubt, a day of reckoning will come if market principles are allowed to work out their natural balance. However, the moneychangers

design a fantasyland of monetary assessment that distort and prop up the price of the "Reserved Currency". John Plender writes in the Financial Times, Central bank hot air pumps

up bond bubble, presents an analytical evaluation of worth in the current bond values. "In the

fixed interest sector something irrational is undoubtedly going on, but it is less a matter of exuberance than desperation

in the pursuit of yield. In higher yielding parts of the market prices are out of touch with default risk. Despite the oft-heard central bankers’ refrain that bubbles are impossible to identify

until after they have been pricked, historical comparisons leave little doubt that this is a bubble – one, moreover,

to which central banks have contributed their fair share of hot air. It is rare indeed for investors to pay a multiple of

more than 50 times for the income stream on a 10-year Treasury bond."

Nevertheless,

this inflated bubble just keeps expanding from the unlimited flow of repurchases by the Federal Reserve of Treasury debt.

What else is left to do, when the global financial markets are reluctant to buy into the next round of T-Bill offerings? Indefinite

aggressive QE is here to stay as long as the need to roll over the debt exists. This view is shared in the latest report,

Treasury Bond Bubble Will

Not Pop, Fed Will Simply Increase QE. Guru Jim Sinclair offers the conventional-politicized viewpoint that the

printing press will just keep running. "Essentially Sinclair is stating that interest rates will continue to manipulated at

an artificially low level by uneconomic buying of T-bonds by the Federal reserve governor typing on a keyboard, and that the

pace of QE will keep pace with the pace of the US budget deficit/ funding gap, until which point the US dollar faces a collapse

in the confidence of the currency itself."

Of course,

the operative circumstance is when will the collapse of the Dollar currency come? The interest rates charged to purchase T-Bonds

will rise, when the Fed decides that the underreported rate of inflation can no longer be concealed from institutional transactions.

When the Street panics over, the artificially low levels on Treasury Bonds rates, and refuse further purchases, the international

exchange rate of the Dollar will plummet. The global rush to devalue

currencies is in full force and over time will affect the options that the Fed has in their toolbox. This chicken and egg

dilemma will test the legal tender equation to its core. While the government can coerce the acceptance of a failing currency

to be used as money, the same cannot be inferred about the purchasing power of T-Bonds. The

linkage between the underlying capital used to purchase the government note and the final return received for holding the

bond until maturity has a profound disconnect. Selling your T-Bonds is a wise practice even if an imminent bubble is not ready

to blow. The harm to the financial markets from another precipitated

house of cards should scare everyone. Expectations have a funny way of influencing financial results more often than sound

evaluations. The prospect of a default by the Treasury is embedded, even under synthetically low interest rates. Just how

long will this anticipation hold true? James Hall – February 13,

2013

Discuss or comment about this essay on the BATR Forum

|